If I had to answer that question in one word, the answer would be – nothing. No, really the Union budget 2018 means nothing for the salaried middle class.

To say that this budget is disappointing for people like us would be like saying it rains in Mumbai – an understatement of huge proportions. It provides salaried folks with literally no benefit but seems to be taking more money out of our pockets.

I have spent years reading through the budget, getting confused with the macroeconomic terminology and wondering how it impacts my life. With Elementum Money, I wanted to eliminate the trouble of doing that for my readers. So, here are the main points of the budget that will now change things for you.

INCOME TAX EXEMPTION

- Introduction of a standard deduction – Rs. 40,000

Starting this year, the government has now introduced a standard deduction for taxable income. That means, every one can directly deduct Rs. 40,000 from the income number before arriving at the taxable income.

Before you start jumping for joy, know that this comes in lieu of the conveyance allowance and the Medical reimbursements that are already at Rs. 19,200 and Rs. 15,000 respectively. This new rule only means an additional standard exemption of Rs. 5,800 where the maximum additionally saved budget would be approximately Rs. 1,810.

What it also does is simplify the process of tax declaration proofs for the deduction. You no longer need to pay the neighbourhood pharmacy that extra bit to make you bills at the end of the year.

- Senior citizen health insurance exemption hiked from Rs. 30,000 to Rs. 50,000

Under Section 80D, the limit of exemption for health insurance premium for senior citizens is currently Rs. 30,000. This could also be claimed by a tax paying child if the premium was in the name of the senior citizen.

Now, the exemption for health insurance premium for senior citizens has been raised to Rs. 50,000 and rightly so considering their premiums are higher. However, through my readings it has been unclear if tax paying children can claim it or not.

Also, for some specified critical illnesses, tax exemption has been hiked on expenses up to Rs. 1,00,000 which was currently at Rs. 60,000 for senior citizens and Rs. 80,000 for Super Senior Citizens.

- Interest income exemption increased from Rs. 10,000 to Rs. 50,000 for Senior Citizens

One of the best outcomes of the budget is the hike given in income tax exemption to senior citizens for interest income from bank deposits. This includes Fixed Deposit and Recurring Deposits.

This is a great move considering a lot of their wealth is in risk-free instruments like FD and an increase in tax exemption for this much needed. They have also done away with TDS (Tax deducted at source) on bank deposits for senior citizens.

INCOME TAX PAYMENT

- Increase of cess on income tax from 3% to 4%

This is a big one, according to me. If you thought the government gave some income tax relief with the standard deduction, it is taking much more out of your pocket.

In case you are scoffing, wondering how can a 1% hike make a big difference, let me give you an example. Let’s assume person A has to pay Rs. 2,00,000 tax. Mind you, a lot of us must be paying even more than that. If he earlier paid Rs. 6,000 cess, he now has to pay Rs. 8000. That wipes out most of the Rs. 3,000 benefit of the deduction and in a lot of cases will be much more paid.

INVESTMENTS

- 10% Long-term capital gain (LTCG) on Stockholdings

As a promoter of getting more Indians to start investing in equities, this was the most dismaying part of the budget announcement for me. To confuse people further, this announcement comes with a lot of terms and conditions.

If any of you are familiar with the concept of LTCG (be it in real estate or in bonds), you would know it mostly comes with the concept of indexation. The government allows you to fight inflation tax-free and anything above that is taxed. So, indexation numbers are released for every fiscal year and the ratio between the numbers in the years of acquisition and sale are considered. The same ratio is applied to the acquisition price and the excess is taxed.

However, in this rule, any gains above Rs. 1 Lakh in a financial year will be taxed at 10%. To add to that, they have also put in a clause of grandfathering gains made till Jan 31, 2018. That means that if you have been holding stocks for more than year till Jan 31, 2018 then the acquisition price or the closing price on Jan 31st will be considered as base price. Confused? Even I was, till I read this.

Let me explain with an example.

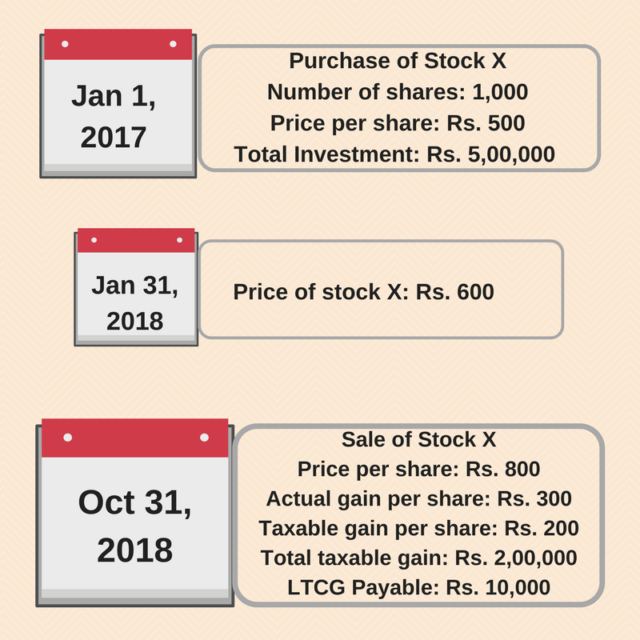

Suppose you buy 1000 shares of Stock X on Jan 1, 2017 at Rs. 500 per share (Total investment – Rs. 5,00,000). The stock price on 31st Jan, 2018 has risen to Rs. 600 per share.

You decide to sell all your 1000 shares on Oct 31, 2018 seeing the stock price touch Rs. 800 per share.

While your real gain is Rs. 800 – Rs. 500 = Rs. 300 per share, for taxation purposes, it will be calculated as Rs. 800 – Rs. 600 = Rs. 200 per share. This is because you were eligible for the grandfathering clause.

So, the total gain is taken to be Rs. 2,00,000 (Rs. 200 per share for 1000 shares). Of this, Rs. 1,00,000 is tax-free. On the remaining Rs. 1,00,000 you are due to pay 10% which would be Rs. 10,000. (Note: The first Rs. 1,00,000 on which you do not have to pay tax applies for gains in the entire financial year).

In my opinion, hoping for a reversal of this rule in the next year might work better.

- 10% Dividend Distribution Tax on Dividend Mutual Funds

There are 2 types of Mutual Funds one can invest in – Growth or Dividend. Growth funds reinvest any divided received from stock holdings.

Dividend funds end up paying mutual fund holders the proceeds at regular intervals as and when their stock holdings announce and process the divided. Currently, the distribution of the said dividend is tax-free. Thanks to this ruling, it will now attract a 10% dividend distribution tax.

This has been done with a stated intention of putting dividend and growth mutual funds at par.

Industry experts opine that this could lead to Mutual funds pushing the growth schemes more and worse it could end up disheartening some of the early small investors.

INDULGENCE

- Custom duty on mobile phones increased from 15% to 20%

Mobile phones will be more expensive with the hike in custom duty

One of the indulgences for a lot of us is our mobile phone and most of the devices are imported. This budget ensures that this indulgence costs just a little more by increasing the custom duty on the devices from 15% to 20%.

So, what are your thoughts on Budget 2018? Drop a comment below or email me at aparna@elementummoney.com

Take your first step today. Sign up for the Elementum Money Weekly Newsletter to download the Financial Feminist checklist. Also,get nuggets of financial wisdom with our 3 posts every week, directly to your inbox. Have more questions, feel free to send any of them my way at aparna@elementummoney.com.

Related Post:

Leave a Reply