In whatever money conversations I have had till date, I have realized that credit cards still seem to be an elusive subject.

In one of the consumer research that we had conducted among millennials, there were quite a few who had sworn against using them for fear of over-spending while one guy used his card to swipe for his room-mates to get the card offers and for the reward points himself.

Personally, my first interaction was when my father took his first credit card when I was a teenager. At that time, he was one of the few people to have and use a credit card and acceptability among merchants was pretty low.

I believe we have come a long way now. I have now used Credit Cards of the 3 largest Indian private banks in the last 8 years.

Credit cards are a convenient way of using money. Fear comes into the picture when we don’t know the product well enough.

But as I like to put it out here – Have no (financial) fear, Elementum Money is here!

Read all you need to know about credit cards and download the handy infographic at the end.

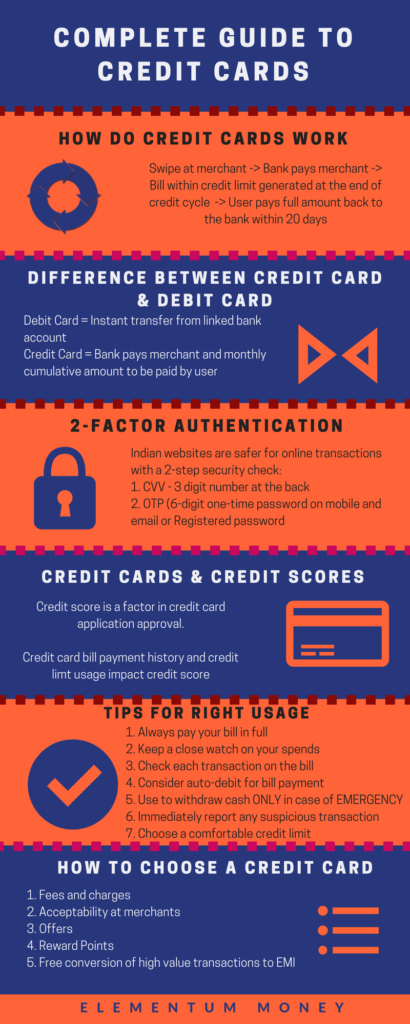

How do credit cards work?

Credit cards, as the name suggests are an instrument to provide short-term or a 20 – 50-day credit to the user. Considering this jargon can be confusing, let’s look at an example.

You have an SBI Credit Card with a credit limit of Rs. 1,00,000 per credit cycle. Your credit cycle is from 11th of a month to 10th of the next month.

Suppose you are out shopping at Big Bazaar on 11th June and make a purchase for Rs. 10,000 by swiping your SBI Credit Card. SBI will pay Big Bazaar Rs. 10,000.

Your bill will get generated on 10th July. Assume you get a bill of Rs. 60,000 for all the purchases you made using the card in the period from 11th June to 10th July. You will then have an additional 20 day period until 30th July to pay that bill in full.

Difference between Debit Card and Credit Card

Debit cards result in an instant transfer of money from your account as per the transaction whereas, with a Credit Card, you pay the bill 20 days after the end of a credit cycle.

So, in the above example, had you swiped for that transaction using a Debit Card, the amount of Rs. 10,000 would have been instantly transferred from your linked bank account to Big Bazaar.

Personally, I have always found that to be a risky proposition and use a Debit Card only to withdraw cash from ATMs.

The fact is cards are always a security threat. However, in case of a Credit Card, you can file for fraudulent charges without money ever leaving your account. If your Debit Card ever gets compromised, the soup that you land in would be hotter and more stressful.

2-factor authentication

Ever heard this term and wondered what the hell does it mean anyway?

India is one of the few countries where online transactions have double security built in. When you make an online transaction on an Indian website, even if you save your Credit Card details (16-digit card number, Expiry date of the card, full name as on card), you will still be required to key in inputs twice.

The first thing you will be asked for is CVV which stands for Card Verification Value. CVV is the 3-digit number right next to the signature panel at the back of the card. This is a security feature to confirm that you have the card with you.

The second check is when you submit all these details and you are asked either for a password or an OTP. In this case, one of the options is to register on the Visa or Mastercard website (according to the logo on your card) and choose a password which you then key in whenever prompted during an online transaction.

In the other route, you will be asked to re-confirm your contact details (masked registered phone number and email ID. Once confirmed, you will get an OTP or a One-Time Password as an SMS on your phone and on your email.

While hard to believe, Indian websites are actually safer when it comes to financial transactions. Most foreign websites do not have this security feature making it easier for card details to be hacked.

Credit cards and credit scores

Did you know credit cards and credit scores are closely intertwined?

Your credit score and credit history is a big factor in the approval process of your Credit Card application. After all, for the bank, it is an unsecured loan.

That’s not all. If you don’t pay your credit card bill on time, it negatively impacts your credit score in a big way. How much of your credit limit you use every month also influences your credit score. The lesser proportion of credit limit used, better it is for the health of your credit score.

Tips to ensure right usage of cards

If you think, I have been painting too rosy a picture of credit cards, now is when I give you a reality check on it.

Credit cards are like alcohol – when used responsibly in moderation, they can make your (financial) life better. Click To TweetSo, here are some tips from my 8 years of intensive use of credit cards:

1. ALWAYS pay your credit card bill in full

If you are a credit card user, you would know how every month banks end up sending a misguided message – your credit card bill – 20x, minimum due – x. Unfortunately, a lot of users end up thinking it is ok to just pay the minimum amount. It is NOT!

If you pay just the minimum amount on your bill due, the balance amount is considered to be revolving credit with an interest rate of 2-3{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} per month! If you necessarily need funds, plan in advance and apply for a personal loan which would be much more cost-effective.

2. Keep a close watch on your credit card spends

In India, for every transaction on your credit card, you are bound to get an SMS alert. At the end of the alert, the SMS also mentions the available limit. This refers to the remaining limit on your credit card in the ongoing cycle.

For instance, in the Big Bazaar example above, if the Rs. 10,000 is your first spend in the particular credit card cycle, and the card limit is Rs. 1,00,000, the transaction alert message will then specify – Available limit – Rs. 90,000.

Why such an elaborate mention of the transaction SMS? Well, one practice I follow is to ALWAYS check the credit limit in every such SMS to do the maths of what I have spent in a month on the credit card. If need be, find your own trick to keep a watch on your credit card spends every month so that you do not end up with a rude shock at the end of the month.

3. Check each transaction on your credit card bill

Banks are humans and hence can err. If you use a credit card, one of the responsibilities is to scan the bill every month to ensure all transactions have indeed been made by you.

4. Consider automatic payment for the credit card

You can set up an automatic debit rule for your credit card bill, on the bank account of your choice. If you are comfortable with it, choose a date close to the last bill payment date and set it up to give you enough time to check the bill and clear any dispute if need be.

Personally, I have still kept my credit card payment on a manual setting where I transfer money through the mobile app while the husband has set up his card for automatic debit.

5. Use a credit card to withdraw cash ONLY in case of a DIRE financial emergency

A credit card’s purpose is only digital transactions. If you do withdraw cash using your credit card, you pay heavily for it – 2.5{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} at the time of withdrawal and 2-3{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} per month until the time of repayment!

So, if you withdraw Rs. 10,000 using your credit card, you pay Rs. 250 as a transaction fee and around Rs. 200 – Rs 300 every month that you do not pay.

6. Immediately report any suspicious activity on your card

Some years back, while single and living along, I was up late at night watching a movie on my laptop. Suddenly, I got an SMS on my phone about a transaction on my credit card.

Without a moments’ hesitation, I called up the phone banking for the card and got the card blocked immediately with a request for a card replacement. I also filed the case for a fraudulent transaction.

Always read your credit card transaction SMS to confirm the amount and at the hint of a suspicion, take appropriate action.

7. Choose a credit limit that you are comfortable with

This month, again I had two fraudulent transactions on my credit card (different bank though). The immediate blocking of the card helped me to limit the damage. However, the attempted fraud happened during waking hours.

So, while my credit card offered a card limit of Rs. 2,00,000 following this instance, I reduced it to Rs. 75,000 considering most months my credit card bill is less than Rs. 25,000. I prefer peace of mind to having an unnecessarily inflated credit limit.

How to choose a credit card

1. Fees

Typically, credit cards come with an issuance as well as an annual charge. Today, there are a lot of credit cards that are either free of that charge or give an offer to compensate that charge. For eg, if you pay Rs. 1000 as an issuance + first-year fee for a card, the company might be offering a Rs. 1,500 travel or shopping voucher.

Then there are some cards that waive the annual fees on the basis of the quantum of your spends in one year.

Check for the conditions on the charges of your card and go for one which suits you best. Personally, I go for the free credit cards, no strings attached.

2. Acceptability

Today most big retailers and even the smaller shops accept credit cards. However, most retailers accept only Visa, Mastercard and in some cases Rupay card.

While American Express has a name in premium credit cards, the acceptability is still not wide enough to make it a convenient choice. If at all, it can be a second credit card.

3. Offers

One of the biggest draws of credit cards are the offers they come with. Citibank and it’s cards gained in popularity and number of users thanks to the fantastic dining offers they became known for.

Today, most credit card companies view or the wallet share of the customer by one-upping on the offers. One of the most common? Cashbacks, where you swipe at a retailer and get a percentage of the amount back in your card account after some time. Word of caution, most of these offers come with plenty of conditions. Read it completely to know for sure how to really get the offer.

Don’t get misled by the fancy names of the credit card. Check for their always-on offers and then take a call.

4. Reward points

With every swipe of your credit card, you end up earning reward points which when accumulated to a sizable chunk can be redeemed for selected vouchers.

While some banks now offer reward points on every transaction, the quantum of points generated is generally higher for credit card usage.

Whichever credit card you might choose, check the reward catalogue and ensure there are some vouchers you do like and would want to redeem for. For instance, recently I redeemed some of my credit card points for an instant online voucher of Bookmyshow and voila! The husband, my parents and I watched Tiger Zinda hai for 50 bucks in PVR.

5. Free EMI

A lot of credit cards give an option of converting high amount purchases to EMI at 0 cost, that means 0{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} interest. It’s a handy feature to have as breaking up a big purchase into smaller chunks can always help your cash flow, if it does not come at a cost.

It ’s a feature often used by my husband.

Now that you know that credit cards are not the scary monster you thought they were, do some research, apply for one and start using it. You can either check the website of a bank of your choice and call them up or you can apply to an aggregator site like Paisa Bazaar or Bank Bazaar to be inundated with calls.

Educate and empower yourself for a better financial life 🙂

Take your first step today. Sign up for the Elementum Money Weekly Newsletter to download the Financial Feminist checklist. Also, get nuggets of financial wisdom with our 3 posts every week, directly to your inbox. Have more questions, feel free to send any of them my way at aparna@elementummoney.com.

Leave a Reply