Have you been toying with the idea of life insurance for some time? You have probably even crawled some of the aggregator sites, looking up all types of articles for help but that has just left you even more confused.

You might be convinced on the idea of term insurance, but how much do you need? How do you even arrive at that number?

That figure of Rs. 1 Crore often touted by insurance companies as a minimal figure is something that has left you befuddled. All you are looking for is some logic to finally zero in on the number to buy a life insurance policy. You figure that you can always increase the cover in case there is a major event in life, but atleast to start the process you need to know how much life insurance to buy.

You have landed at the right place. Today I am going to tackle the tricky question of how to arrive at the appropriate life insurance amount considering various factors and scenarious. So, here it is – a one stop destination of all possible ways to calculate the amount of Life Insurance cover that you might need:

RULES OF THUMB

This I believe is the most popular way, for obvious reasons. Rules of thumb work because they are easy to calculate and somewhat do the job, even if it might be inaccurate to quite a degree.

Some of the common rules of thumb are:

- Income Rule – This rule is just about having a life insurance amount worth 8-10 times your annual gross salary. While it is easy to calculate, this method does not have a very strong logical reasoning behind it. Also, it does not take into account specific financial details of the person like any loans or differences in spending etc. If the person was earning 15 Lakh then he ends up taking a cover of Rs. 1.2 – 1.5 Crore

- Premium Rule – This rule, in my mind, misses the point altogether. The idea behind this rule is figure out how much one can afford to pay as premium from his/her disposable income and check the possible cover with that premium. This inverted approach can end up in relegating life insurance to the end of the priority list or buying excessive unnecessary insurance. Another approach to the same rule says 6{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} of one’s gross income should be spent on insurance premium + 1{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} for each dependent. In case someone has 3 dependents that actually comes to 10{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} of the gross income, which might really not be required.

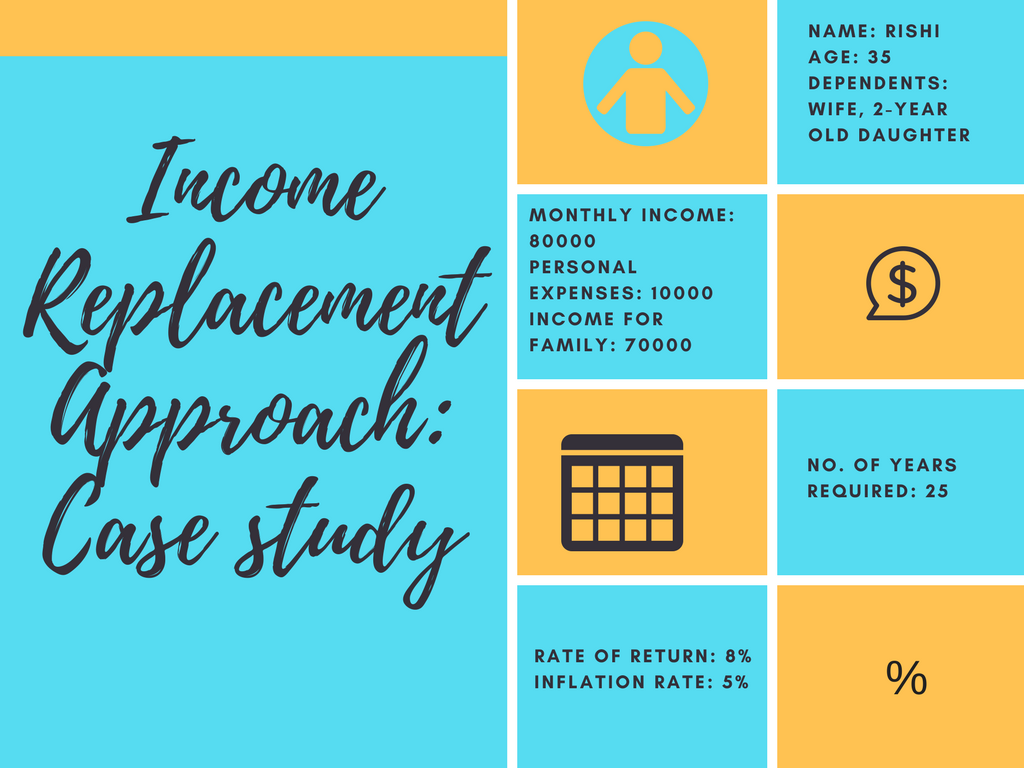

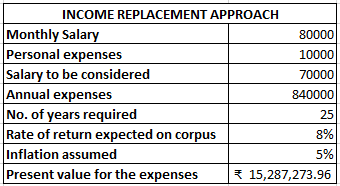

INCOME REPLACEMENT APPROACH

This calculation takes into account the net income currently earned by the bread winner and not spent on himself, spread out over his working life and discounted to see what it would mean in current terms. Ok, don’t look so befuddled. Let’s look at an example.

Rishi is 35 years old and works in an IT firm. He is married and has a 2-year old daughter Ashna. His net post-tax monthly salary is Rs. 80,000 of which he spends Rs. 2000 a month on the life insurance premium and around Rs. 8,000 ends up being spent on personal expenses like clothes, eating out etc. So, Rishi ends up earning Rs. 70000 for his family every month, which would mean Rs. 8,40,000 every year. He expects to work till the retirement age of 60, which means he has 25 years of income producing life left. If I simply multiplied the annual economic life, then the cover would come to Rs. 2.1 Crore.

However, we have forgotten to take into account a very important factor – time value of money which is a double-edge sword.

Time value of money will mean that you would invest your lumpsum in an interest bearing instrument, even if it is risk-free like a long-term debt fund or a Fixed Deposit. It is assumed that growth can be used to discount the value of money in current terms.

However, time value of money simultaneously implies that each rupee is getting cheaper thanks to the steep inflation. Every year the 8,40,000 that the family would get will end up covering lesser of their needs. So, an appropriate discounting factor would take into consideration the rate of return on the lumpsum money as well as the rate of inflation required to be able to meet the financial needs. To calculate that, Microsoft excel is a particularly useful tool.

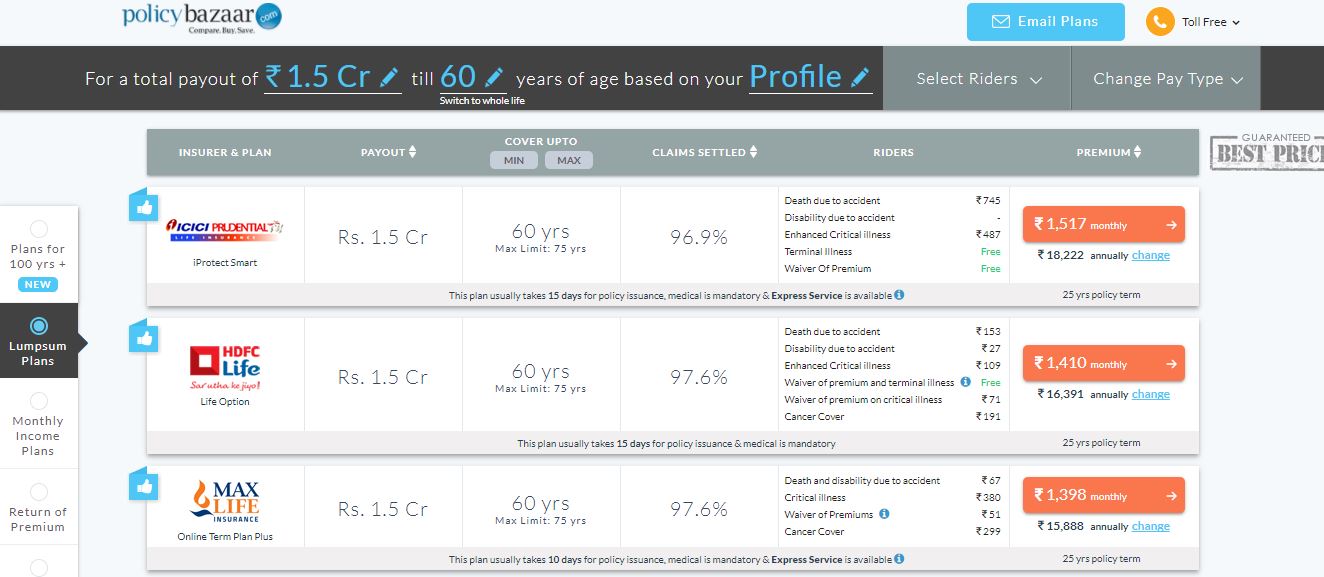

On discounting, if you consider 8{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} as your rate of return (current average returns for long term debt funds) and 5{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} as the rate of inflation, the insurance cover required reduces to about Rs. 1.53 Crore. Check the calculation with the life insurance calculator.

Download the life insurance calculator to calculate your appropriate life insurance cover.Calculators for Life Insurance Policy

If you consider only term insurance, the per month outlay for such an insurance is not as high as often assumed. Below are the quotes of a few of the Life Insurance providers as popped up by Policy Bazaar for a 35 year old male non-smoker.

NEEDS APPROACH

You might want to grab a cup of coffee before we dive into this one. Unarguable the most complicated but also the most logical and scientific approach to calculating the appropriate Life Insurance cover.

The needs approach covers you for all things that you would have needed money for – living expenses, outstanding loans and financial goals. However, it is not only the insurance which pays for all of these as the insurance cover needs are taken into consideration after reducing any accumulated assets.

Don’t zone me out just yet. I am going to detail out what I really mean in readable English.

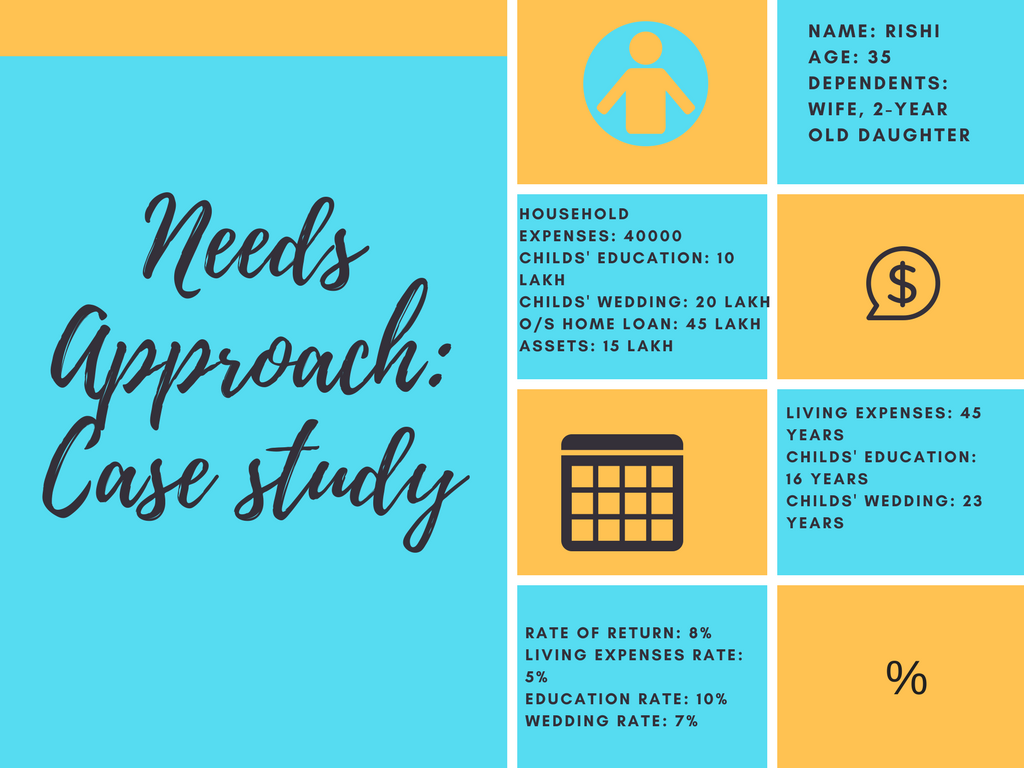

Let’s continue with the Rishi example. As a recap,

Age: 35

Family: Wife and 2-year old daughter Ashna

Monthly net salary: Rs. 80,000

Current monthly household expenses: Rs. 40,000 (If his wife is earning, he can look at taking a lower number which is contributed directly by Rishi)

Rishi assumes his wife’s life expectancy to be 80 years and would like to provide for these expenses through her lifetime.

Outstanding Home Loan: Rs. 45,00,000

Rishi also realizes that he has some aspirations for his kid like education and wedding. He puts a number to it:

Education @ 18: Rs. 10,00,000 (Current costs)

Wedding @ 25: Rs. 20,00,000 (Current costs)

Before taking a life insurance policy, he checked his Employee Provident Fund balance to realize that it had a neat Rs. 10 Lakh saved and over the years he has also bought gold which is worth Rs. 5 Lakh today.

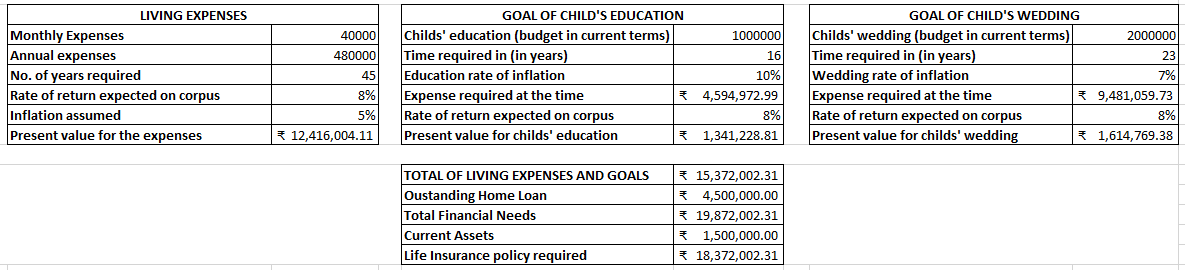

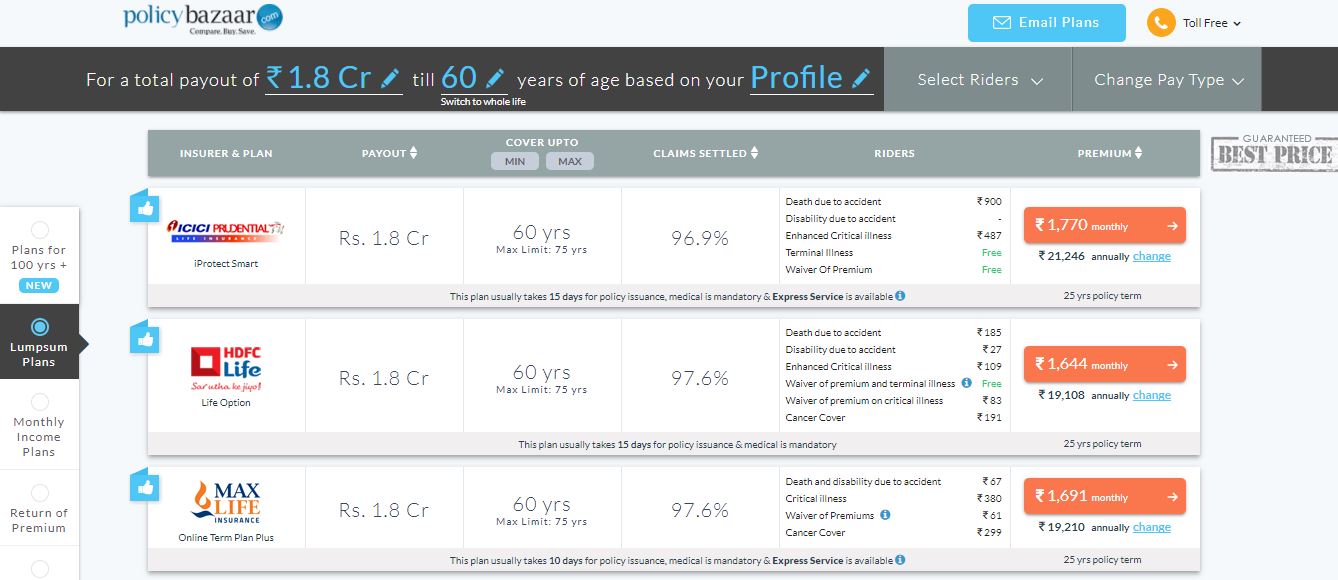

Now, when Rishi decides to buy a life insurance policy, he know what all he is planning to accumulate money for. Assuming a uniform rate of return of 8{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} on the lumpsum money and varied inflation rates, you can easily arrive at the appropriate amount of life insurance best suited for your particular needs. For the financial goals, considering it is a lumpsum required, calculate the inflated value before discounting it as per the expected returns. In this case, Rishi should opt for almost Rs. 1.85 Crore. Check the calculation with the life insurance calculator.

Download the life insurance calculator to calculate your appropriate life insurance cover.Calculators for Life Insurance Policy

I checked on policy bazaar by increasing the amount of life insurance to the 1.85 Crore required and yet again the policies come to very reasonable amounts. I would say it is a very fair price for peace of mind.

LIFE INSURANCE FOR HOME MAKERS

For quite some time I did not really understand or see the need for life insurance with home makers. The more I read, the more I nodded my head to the core reason of money needed to substitute the tasks that these women accomplish out of their love. Consider the following case:

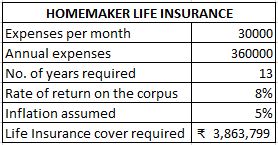

Shiela is a 38-year old woman, happily married to Bala and is the mother to an 8-year old son and a 5-year old daughter. She is a stay-at-home mom. On a typical week-day, she packs their lunch and helps them get ready for school. After school, the kids come straight home. In the evening Shiela drops them off to music classes and with the help of a maid has the dinner ready at home. She then picks up the kids and is back home by the time her husband also comes back.

In case, Shiela has an unfortunate accident which leads to her demise there are a few new financial expenses for Bala to consider. This would include a full-time maid and a driver as minimum pre-requisites. Considering Rs. 30,000 per month for this till the time his daughter is an adult (13 years), it will still mean the requirement of a life insurance of almost Rs. 40 Lakhs (Considering an 8{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} return on the corpus and 5{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} annual rate of inflation). A snapshot of the calculation is given below. Check the calculation with the life insurance calculator.

Download the life insurance calculator to calculate your appropriate life insurance cover.Calculators for Life Insurance Policy

If you are thinking – this makes sense but there are too many zeros here and the numbers are still swimming around my head, feel free to contact me and I would be happy to help work out with you for an appropriate life insurance policy or the amount of cover required. Do let me know your opinion in the comments below or email me at aparna@elementummoney.com

Other posts in the #LIMonday Series:

Why do you need Life Insurance

Leave a Reply