A few months back, a guy on my college friends Whatsapp group sent the following joke:

A person to his friend: My wife’s credit card got stolen 2 weeks back.

Friend (with concern): I hope you got it blocked

Person: No. The thief spends much less than my wife!

This joke was a perfect trigger to my feminist tendencies and I protested, “That’s a sexist joke!”.

However, what made me really angry was when another girl in the group quipped, “But this is the truth Aparna. We women spend so much more than men and there are so many more avenues for us to spend.”. Granted she was the joke-posting guys’ wife but if we women are the ones to promote such stereotypes, then god save us all.

For generations, women in India have been the finance controller of households. While consumerism and opportunities to spend might have exploded in the last few years, it takes nothing away from the innate financial sense that women possess.

Which brings me to the topic that I am addressing today. Why do women shy away from investing? Stock markets are one of the easiest places to start investing in (for reasons like low entry ticket size, fairly liquid). It is then a commentary on us as a financially gender unequal society that only about 24{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} of the 1.09 Crore demat accounts held by CDSL (Central Depository Services Limited) were those of women. This would include enough inactive and dormant accounts as well as those operated by others (rather than the holder herself).

I myself have resisted for over 4 years, my father’s not-so-subtle nudges to start investing while finally taking the plunge only little over 2 years back. Recently, through my work I was part of primary research where some young women were invited to discuss their lives, money and banking. From these 2 experiences, I have tried to glean some excuses that we women might make to not invest and why those excuses are really invalid.

Excuse #1: My father/husband/brother invest my money because men are better at it

If you have someone in your family to invest for you, then it is a great learning ground and that is where it should stop. You should take that opportunity to understand their investing strategy, learn from it, read up some more and then put in your investment strategy in place.

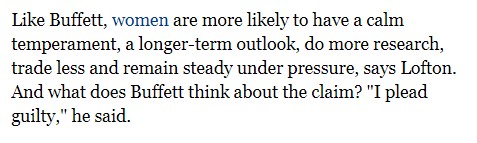

As for the “men are better at investing” you must read the book – “Warren Buffet invests like a girl” by LouAnn Lofton. In the book, Lofton concludes that Warren Buffet’s investment style shares a lot with traits shown by women investors (as brought out by research). Forbes Magazine describes it as such:

Wells Fargo Investment Institute in their recent research about women investors also talks about the 3 most important traits that make women more successful – Patience, discipline and willingness to learn.

A lot us find the complexities in finance and investment to be a put-off

Excuse #2: Finance and investment is complicated

It sure is and the jargon around it does not make it easier. But this would be just one more of the other complicated things that you do with ease in your daily life – be it your job, running a house, raising kids etc. If you can do any of those or more, then managing money and investing it is far easier. As for the jargon, this blog is an attempt to demystify and get more women to invest.

Excuse #3: Money is not important

This is a farce. You are either struggling with keeping tabs on your money and decided that abandoning any feelings towards it is easier or would rather keep this approach than work on a disciplined path towards making money work for you. Start by taking a moment to think, what does money mean to you.

Excuse #4: I don’t earn enough to save

I have used this excuse in the past but now I know I was just running away from investing. Saving is a mindset. You can start with as little as Rs. 500 per month. If that also sounds like too much to put aside, start putting a Rs. 20 note in a piggy bank every day the way we did when we were kids. Gradually you will build up on the “habit” of saving and it will become effortless.

Too many women harbour the misconception of not being good with numbers

Excuse #5: I am not good with numbers

We women lack in just one thing – confidence in our own abilities. This is not just an Indian phenomenon but rather a globally seen trend. Wells Fargo Investment Investment Institute conducted a study a year ago (Aug 2016) which showcases the fact that women have less confidence in their investing skills than men even though the same study shows that the results of women investing show a lower variability than men.

This is one of the core stereotypes that we should fight against, at least in our heads. In this respect, Always (the sanitary napkin) did a fantastic social experiment #LikeAGirl in the UK to show that such stereotypes affect girls only after the age of about 12, when their self-confidence really starts dropping. What can we do to bring that confidence back?

Excuse #6: I would rather spend my money than wait to spend it

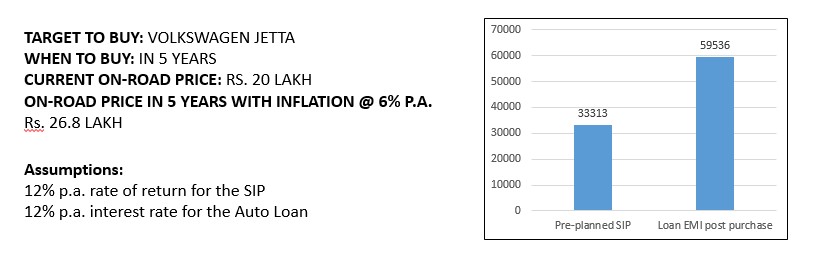

Ah, the instant gratification syndrome. As a kid, I used to get a monthly pocket money and for big-ticket purchases, I had to save it up to buy. Even today, there are times when the constant armchair travel for an upcoming holiday is more rewarding than some of the tiring experiences on the actual holiday. Not just that, financially it is a far better deal too. Let me explain with an example where you can buy a Volkswagen Jetta in 5 years either by investing in a Systematic Investment Plan (SIP) starting today or take a loan for the full amount while buying the car:

In those 5 years, you could even end up rationalising your purchase decision from a Jett to a Polo!

If planned in advance, a big purchase can prove to be far cheaper by putting your monthly payments in advance rather than with a loan. Quite a sweet deal, huh?

While cash is good, it does not protect against inflation

Excuse #7: Cash in accounts and deposits better than risking my money

Yes, market investments are subject to risk. But, if you are otherwise willing to risk eating street food, to use the crumbling public transport that our cities offer, to cross the road, to breathe the dirty pollutant-laden air, to go in a crowded space which could at any time be a terrorist attack target, why would you not invest? Each and every act that we do in life comes with an element of risk and investing is no different. However, if done with some research and care, investing does hold out the possibility of enough benefit to counter the risk.

The average rate of inflation over the past ten years has been approximately 8{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886}. At the same time, the interest rate on term deposits for a period of 1 year has never gone above 9.5{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886}. Apart from a Rs. 10,000 deduction, if you are in the 30{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} tax bracket, the post-tax rate of return then comes to 6.65{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886}. In effect you end up losing money to inflation if term deposits are your only instruments of investment.

Excuse #8: Retirement is far. I will invest for it later

Oh no, you didn’t just say that! While most Indians are woefully behind on planning and saving for retirement, the need to do it is much higher for women. A Mint article (March 2017) cites an Accenture research to put the number at men earning about 67{76b947d7ef5b3424fa3b69da76ad2c33c34408872c6cc7893e56cc055d3cd886} more than women in the Indian workforce. This can be seen thanks to men being the more prominent gender in top management roles. Added to that women live longer than men – A 2014 UN report shows a 5-year gap in the life expectancies of the 2 genders.

To me, these 2 facts imply that women need to have a better retirement corpus. No better time than now to start putting in that money for a comfortable retired life.

Long term or even automated investing requires little enough time for anyone to put into it

Excuse #9: I don’t have the time to invest

This was one of my favourite excuses at some point in time. To me, stock markets meant constantly being online ready to click on the “buy” or “sell” buttons at the minute some hot news or tip makes itself known. However, now that I have started investing it’s clear that with more active investing you are riding on the confidence that you can time the market and beat the index.

This confidence is not only misplaced because a number of studies show you cannot time a market but it also comes with its own costs – higher brokerage costs with more frequent trades and higher short-term capital gain taxes to pay when you trade within an year. A far more fruitful and prudent approach with respect to time and returns is to thoroughly research a stock, buy good companies at reasonable prices and then stay put.

Still think investing is not for you? Have more excuses or just questions or doubts before stepping into this terrain? Just send them to me on aparna@elementummoney.com or post your comments below.

Leave a Reply